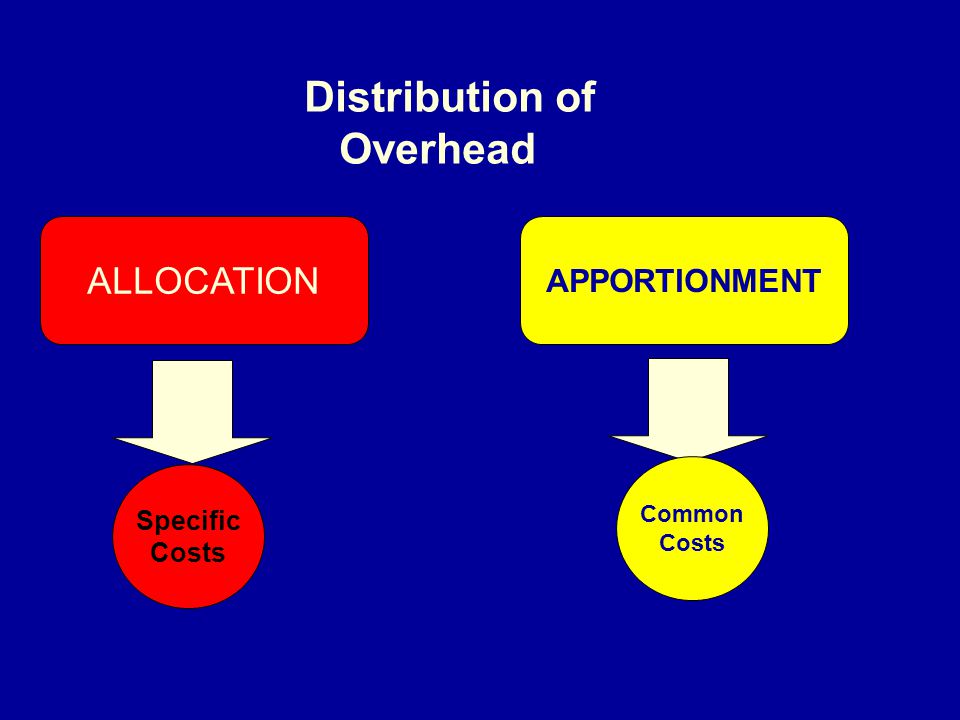

COST APPORTIONMENT

Difference

between service department and operating department:

Most of

the large organizations have both operating departments and service

departments. The central purpose of the organization is carried out in the

operating department. In contrast, service departments do not directly engage

in operating activities. Instead, they provide services or assistance to the

operating departments. Examples of operating departments include the

surgery departments at hospitals, geography departments at universities,

the marketing department’s insurance companies, and production departments at manufacturing

companies like Mitsubishi, Hewlett-Packard. Examples of service

departments include Cafeteria, Internal Auditing, Human Resources, Cost

Accounting, and Purchasing.

The costs

incurred by service departments are usually allocated to the operating departments,

and from the operating departments to the products and services. Many service

departments also provide services to other service departments within

organization. The cafeteria department, for example, provides food for all

employees, including those assigned to other service departments. In return

cafeteria department may receive services from other service departments such

as from custodial services or personnel. Services provided between

service departments are known as interdepartmental or reciprocal

services.

Several

different methods are used to allocate costs of service departments to

operating departments. Regardless of the allocation method that is ultimately

selected, an allocation must be selected for each service department.

Selecting Allocation Base:

Costs are

ordinarily assigned to products and services by using a two stage process. In first

stage, service department and other costs are allocated to operating

departments. In second stage, the costs that have been assigned

to operating departments are allocated to products and services. Here we will

focus on the first stage, in which service department costs are allocated to

operating departments.

In the

first stage, service department costs are allocated to operating departments by

using a unique allocation base for each service department. The

allocation base that is used to allocate a particular service department's

costs should "drive" those costs. For example, the number of meals

served would commonly be used as the allocation base for cafeteria costs

because the costs incurred in the cafeteria are driven to a large extent by the

number of meals served. Ideally the total cost incurred in the service

department should be directly proportional to the allocation base. If the

allocation base increases or decreases by 10%, the service department cost

should increase or decrease by 10% as well. Managers also often argue that an

allocation base should reflect as accurately as possible the benefits that the

various departments receive from the service department.

For

example the most managers would argue that square feet building space occupied

by each department should be used as the allocation base for janitorial

services because both the benefits and costs of janitorial services tend to be

proportional to the amount of space occupied by a department. A given service

department's cost may be allocated using more than allocation base (see examples below).

For example, data processing costs may be allocated on the basis of CPU minutes

for mainframe computers and on the basis of number of personal computers used

in each operating department.

In

addition to explanation of how to select an allocation base, another

critical factor should not be overlooked. The allocation base should

be clear and straightforward and easily understood by the managers to whom the

costs are being allocated.

|

Examples of Bases,

Company Used to Allocate Service Department Costs

|

|

|

Service Department

Landry

Airport ground services Cafeteria Medical facilities Materials handling Data processing

Custodial

services(building and ground)

Cost accounting Power Human resources

Receiving,

shipping, and stores

Factory administration Maintenance |

Ponds

of Landry

Number of flights Number of meals Cases handled ;number of employees; hours worked Hours of service; volume handled CPU minutes; lines printed; disk storage used; number of personal computeRS. Square footage occupied. Labor hours; clients or patients serviced KWH used; capacity of machines Number of employees; employee turnover; training houRS. Units handled; number of requisitions; space occupied Total labor hours Machine hours |

Direct Method of Cost Allocation-Service

Department Costing:

Definition:

Direct

method is accost allocation method under which any of the allocation base

attributable to the service departments themselves is ignored; only the amount

of the allocation base attributable to the operating departments is used in the

allocation.

Explanation:

The

direct method is the simplest of the three cost allocation methods. It ignores reciprocal or inter departmental services (services

provided by a service department to another service department) and

allocates all costs of service departments directly to operating departments.

Even if a service department (such as personnel department) provides a

large amount of service to another service department (such as the cafeteria

department), no allocations are made between the two departments. Rather all

costs are directly allocated to the operating departments, bypassing the other

service departments. Hence the term direct method.

Example:

To

provide an example of the direct method, consider Mountain View Hospital, which

has two service departments and two operating departments as shown below:

|

Description

|

Service Department

|

Operating Department

|

Total

|

||

|

Hospital Administration

|

Custodial Services

|

Laboratory

|

Daily Patient Care

|

||

|

Departmental costs before

allocation

Employee hours

Space occupied square feet

|

RS.360,000

12,000

10,000

|

RS.90,000

6,000

200

|

RS.261,000

18,000

5000

|

RS.689,000

30,000

45,000

|

RS.1,400,000

66,000

60,200

|

Hospital

administration costs will be allocated on the basis of employee-hours and

Custodial Services costs will be allocated on the basis of square feet occupied.

The

direct method of allocating the hospital’s service department costs to the

operating departments is shown below:

|

Description

|

Service Department

|

Operating Department

|

Total

|

||

|

Hospital Administration

|

Custodial Services

|

Laboratory

|

Daily Patient Care

|

||

|

Departmental costs before

allocation

Allocation:

Hospital administration costs

(18/48, 30/48)*

Custodial

service department costs (5/50, 45/50)**

Total costs allocation

|

RS.360,000

(360,000)

-----------

RS.0

======

|

RS.90,000

(90,000)

----------

RS.0

=====

|

RS.261,000

135,000

9,000

-----------

RS.405,000

======

|

RS.689,000

225,000

81,000

----------

RS.995,000

=======

|

RS.1,400,000

1,400,000

=======

|

*Based on

the employee-hours in the two operating departments, which are 18,000 hours +

30,000 hours = 48,000 hours

**Based on the space occupied by the two operating departments, which is 5,000 square feet + 45,000 square feet = 50,000 square feet

**Based on the space occupied by the two operating departments, which is 5,000 square feet + 45,000 square feet = 50,000 square feet

Several things

should be carefully noted in this example. First, even though both the hospital

administration department and custodial services department have recorded

employee-houRS. These employee hors are ignored when allocating service

department costs using direct method. Under the direct method,

any of the allocation bases attributable to the service departments themselves

is ignored; only the amount of the allocation base attributable to the

operating departments is used in the allocation. Note that

the same rules used when allocating the costs of the custodial services

department. Even though the Hospital Administration and Custodial Service

departments occupy some space, this is ignored when the custodial services

costs are allocated. Finally, note that after all allocations have been

completed, all of the departmental costs are contained in the two operating

departments. These costs will be used to prepare overhead rates for purpose of

costing products and services produced in the operating departments.

Advantages

and Disadvantages of Direct Method:

Although

the direct method is simple, it is less accurate than the other methods since

it ignored inter departmental services. This can lead to distorted product and

service costs. Even so, many organizations use the direct method because of its

simplicity.

Step

Method of Cost Allocation:

Definition:

Step

method is the method of allocating service department's costs to other service

departments, as well as to operating departments, in a sequential manner. The

sequence typically starts with the service department that provides the

greatest amount of service to other departments.

Explanation:

Unlike

the direct method, the step method provides for allocation of a

service department's costs to other service departments, as well as to

operating departments. The step method is sequential. The sequence typically

begins with the department that provides the greatest amount of service to

other service departments. After its costs have been allocated, the process

continues, step by step, ending with the department that provides the least

amount of services to other service departments.

Example:

To

provide an example of the step method, consider Mountain View Hospital, which

has two service departments and two operating departments as shown below:

|

Description

|

Service Department

|

Operating Department

|

Total

|

||

|

Hospital Administration

|

Custodial Services

|

Laboratory

|

Daily Patient Care

|

||

|

Departmental costs before

allocation

Employee hours

Space occupied square feet

|

RS.360,000

12,000

10,000

|

RS.90,000

6,000

200

|

RS.261,000

18,000

5000

|

RS.689,000

30,000

45,000

|

RS.1,400,000

66,000

60,200

|

Hospital

administration costs will be allocated on the basis of employee-hours and

Custodial Services costs will be allocated on the basis of square feet occupied.

The step

method of allocating the hospital’s service department costs to the

operating departments is shown below:

|

Description

|

Service Department

|

Operating Department

|

Total

|

||

|

Hospital Administration

|

Custodial Services

|

Laboratory

|

Daily Patient Care

|

||

|

Departmental costs before

allocation

Allocation:

Hospital

administration costs (6/54, 18/54, 30/54)*

Custodial

service department costs (5/50, 45/50)**

Total costs allocation

|

RS.360,000

(360,000)

-----------

RS.0

======

|

RS.90,000

40,000

(130,000)

----------

RS.0

=====

|

RS.261,000

120,000 13,000

-----------

RS.394,000

======

|

RS.689,000

200,000 117,000

----------

RS.1,006,000

=======

|

RS.1,400,000

1,400,000

=======

|

*Based on

the employee-hours in custodial services the two operating departments, which

are 6,000 hours + 18,000 hours + 30,00 hours = 54,000 hours

**Based on the space occupied by the two operating departments, which is 5,000 square feet + 45,000 square feet = 50,000 square feet

**Based on the space occupied by the two operating departments, which is 5,000 square feet + 45,000 square feet = 50,000 square feet

Example

shows the treatment of step method of cost allocation. Note the following three

key points about these allocations.

1. First, under the allocation

heading in the solution you see two allocations, or steps. In the first step,

the costs of hospital administration are allocated to another service

department (Custodial Services) as well as to the operating departments. In

contrast to the direct method, the allocation base for Hospital Administration

costs now includes the employee hours for custodial services as well as for the

operating departments. However, the allocation base still excludes the

employee-hours for Hospital Administration itself. In both the direct and step

methods, any amount of the allocation base attributable to the service

department whose cost is being allocated is always ignored.

2. Second, looking again on the

example, note that in the second step under the allocation heading, the cost of

custodial services is allocated to the two operating departments, and none of

the cost is allocated to Hospital Administration even though Hospital

Administration occupies space in the building. In the step method, any amount

of the allocation base that is attributable to a service department whose cost

has already been allocated is ignored. After a service department's cost have

been allocated, costs of other service departments are not reallocated back to

it.

3. Third, not that the cost of

Custodial Services allocated to other departments in the second step (RS.130,000)in

example, includes the costs of Hospital Administration that were allocated to

Custodial Services in the first step.

Reciprocal Method of Cost Allocation-Service

Department Costing:

Definition:

Reciprocal

method is a method of allocating service department costs to other

departments that gives full recognition to interdepartmental services.

Explanation:

The

reciprocal method gives full recognition to interdepartmental services. Under

the step method, only partial recognition of interdepartmental services is

possible. The step method always allocates costs forward never backward. The

reciprocal method, by contrast, allocates service department costs in both

directions. The reciprocal allocation requires the use of simultaneous

equations. This method is also known as algebraic method and simultaneous

equations method.

Under

this method the true cost of the service departments are computed first with

the help of simultaneous equations and these are then distributed to producing

departments on the basis of given percentage or ratio. Remember that true cost

of the service department means the cost of the service department which

includes original cost of the department plus the share of the other service

department. The main advantage of this method is to have an accurate distributionin

a single step in the distribution summary.

Example:

A company

has two service and two producing departments. The two service departments

serve not only to producing departments but also to each other. The

departmental estimates for the next year are as follows.

|

Producing departments:

A

B

Service departments:

X

Y

|

50,000

40,000

10,000

8,800

|

|||

|

The service departments costs

are to be distributed as under:

Cost of X : 50% to A, 40% to B, and 10% to Y

Cost of Y : 40% to A, 40% to B,

and 20% to X

|

||||

|

Required:

Transfer the service department’s

costs to each other and to producing departments.

|

||||

|

Solution:

Now we solve the given

illustration first using the simultaneous equation method as follows:

Original costs of service

departments:

X

= RS.10,000

Y

= RS. 8,800

After getting the share

from distribution of service departments:

X

= RS. 10,000 + 20% Y

Y

= RS. 8,800 + 10% X

By putting the value of Y in

equation (1)

X

= RS. 10,000 + 20%(RS.8,800 + 10%X)

X

= RS. 10,000 + 1760 + 0.2X

X – 0.02X

= RS. 10,000 + RS.1,760

0.98X

= RS. 11,760

X

= 11760 / 0.98

= RS.

12,000

By putting the value of X in

equation (2)

Y

= RS. 8,800 + 10%(RS. 12000)

Y

= RS. 8,800 + RS. RS. 1,200

= RS.

10,000

|

||||

|

Distribution Summary

|

||||

|

Department

|

Producing

|

Service

|

||

|

Original costs

Distribution of service

department costs:

X

Y

Total departmental overheads

|

A

RS.

50,000

6,000

4,000

-------

60,000

=====

|

B

RS.

40,000

4,800

4,000

------

48,800

=====

|

X

RS.

10,000

(12,000)

2,000

-------

Nil

=====

|

Y

RS.

8,800

1,200

(10,000)

-------

Nil

=====

|

Use

of Reciprocal Method:

This

method is rarely used in practice for two reasons. First, the computations are

relatively complex. Although the complexity issue could be overcome by use of

computers, there is no evidence that computers have made the reciprocal method

more popular. Second, the step method usually provides results that are a

reasonable approximation of the results that the reciprocal method would

provide. Thus, companies have little motivation to use the more complex

reciprocal method.